Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

Total return is the entire amount of income passed to an investor holding a particular security. It annualizes any price change plus any dividends or interest earned over time. By example, an investor paying $100 for a stock, earning $3/yr in annual dividend, and selling the stock for $110 two years later has an annual total return of 8% [($110 - $100) +$3div + $3div) / $100 = 16% / 2 yrs holding period]. For many bond investors who hold to maturity, the total return can be calculated upfront. The acquisition yield determines the annual return, factoring in coupon payments and price movement towards par at maturity. The distinction is important because a bond held to maturity essentially removes market price risk from the equation, making it a less risky asset.

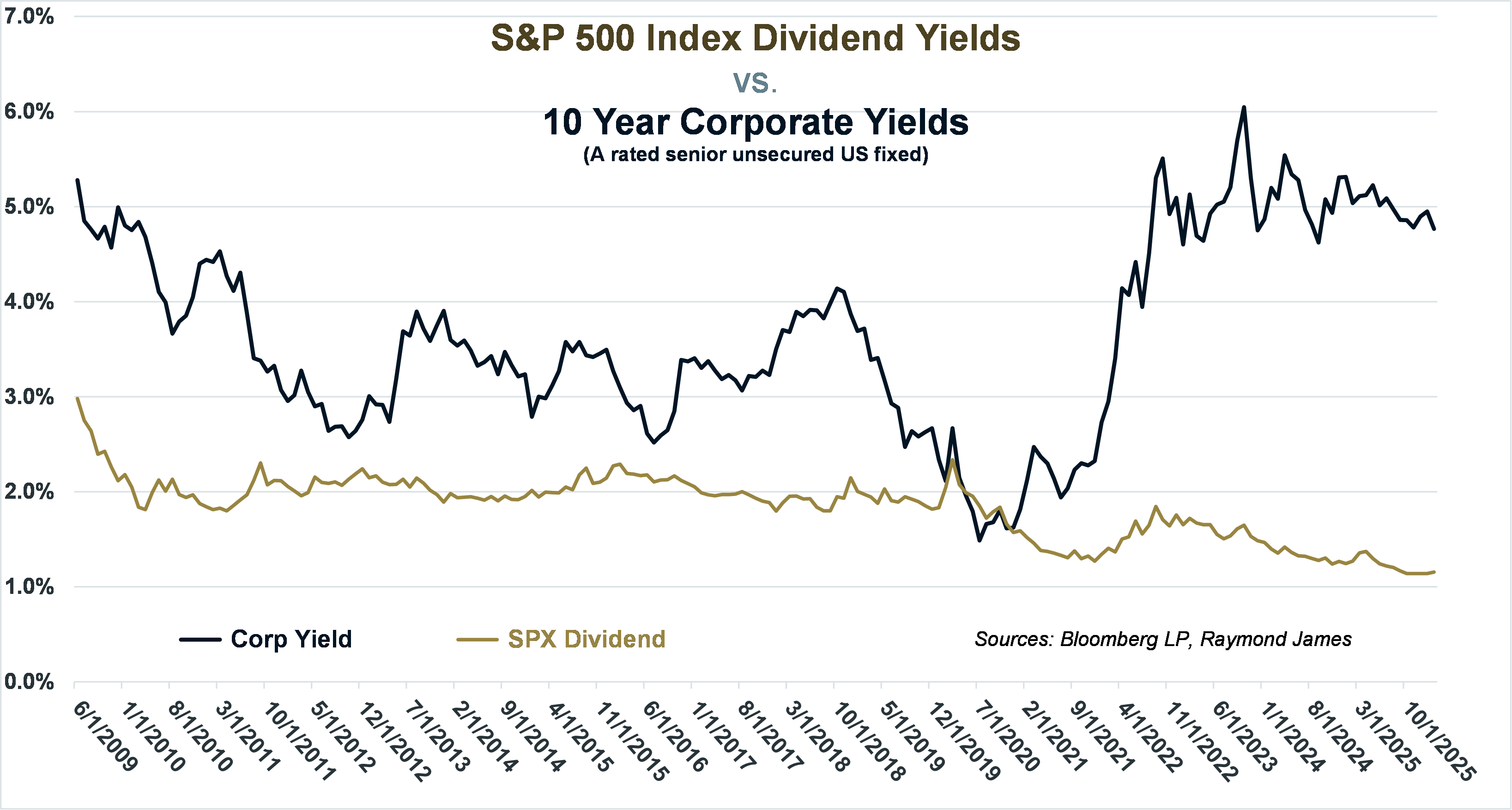

Taking more risk can be both rewarding and costly. Over six of the last seven years, stocks have performed well by providing investors with double-digit returns. The chart shows that, historically, dividend income has underperformed corporate yields. It is rare for dividend income to outperform the average 10-year corporate yields. It is safe to assume that investors seek most of the total return in equities via price appreciation. The robust stock market has enabled many investors to accumulate wealth. Individual bonds may provide investors with a means to lock in a portion of their wealth into less-risky assets at a known return.

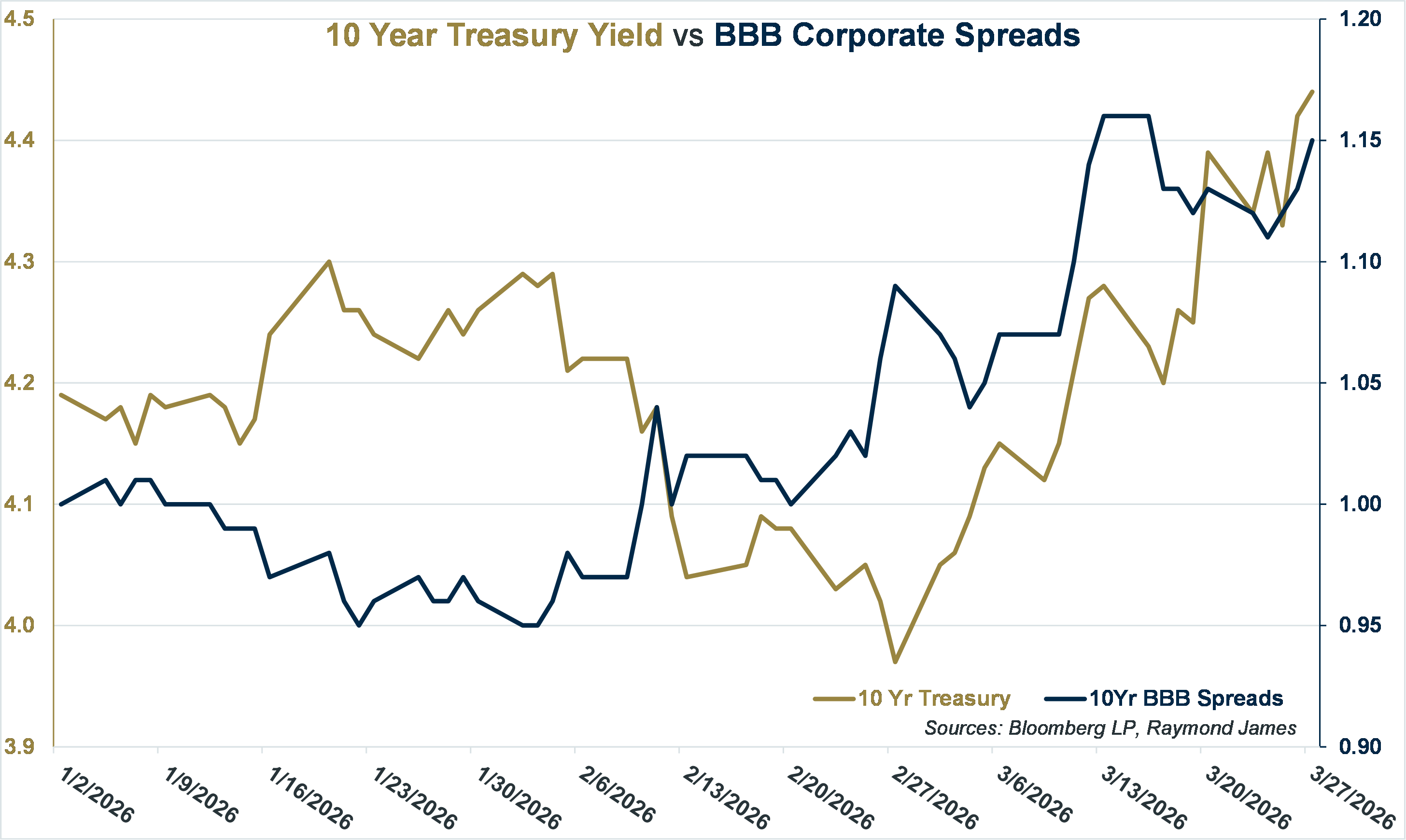

Corporate bonds trade at a spread to Treasury bond rates. If the 10-year Treasury is 4.2% and a corporate bond is at a +50-basis-point spread, then the corporate bond yield is 4.7%. The reason a corporate bond trades with a spread has much to do with real and/or perceived credit risk. The U.S. government is considered more likely to pay its debt. The greater the credit risk, typically the greater the spread or offered yield of a security.

In general, spreads have narrowed to historically low levels since the 2020 pandemic. On their own, narrow spreads indicate investor confidence and a modest risk associated with corporations’ ability to pay their debts. U.S. markets have weathered many geopolitical disruptions better than those of most other countries.

Although still historically narrow, spreads have begun to widen out. What is particularly compelling is that spreads are widening while Treasury rates are rising. For spreads to widen, prices fall, giving pause to total return investors seeking positive price action. However, for buy-and-hold investors, this is exciting news. Higher spreads at a time when Treasury yields are rising translate into higher nominal yields for investors. This provides investors with an opportunity to lock in elevated yields for extended periods and can be accomplished in high-quality, investment-grade individual bonds. It is also an opportunity that comes on the heels of the successful accumulation of stock and housing wealth. Spreads and yields are working for investors.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.