Raymond James Chief Economist Eugenio J. Alemán discusses current economic conditions.

Several months ago, analysts and economists seemed to be convinced that the pass-through from tariffs to higher prices had already occurred. However, new research from the Federal Reserve of New York’s Liberty Street Economics is challenging that view. In a research piece published on July 8, 2026, titled More Tariff Pass-Through Is in the Pipeline, the authors argue that, among all importing firms, 47% of service firms are planning to raise prices during the next year while 44% of manufacturers are planning to increase prices during the same period of time.1

We typically don’t like to bring personal anecdotes into this publication, but some of us have been checking our online bills, and we have seen very large price increases for our subscriptions to newspapers, internet services, streaming services, etc. We typically get charged automatically nowadays, and if you are also in that same boat, check your online charges to see what we are talking about.

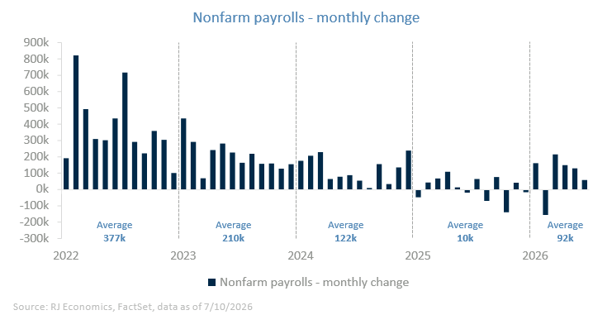

What we are seeing is in line with our argument over the last year that many firms chose not to adjust prices but to adjust the level of employment in order to keep costs contained. This is one of the reasons why we saw employment slowing down from a monthly average of about 121,600 in 2024 to a monthly average of about 9,700 in 2025. This was the immediate response from firms to the uncertainty created by the new tariffs, which seemed to change frequently throughout last year.

While tariff uncertainty hasn’t completely disappeared, it has diminished, and firms are feeling less uncertain about the future. This reduction in uncertainty is showing up in the magnitude of hiring, with average employment growth during the first half of the year accelerating to about 92,000 per month. It is still too early to say whether this employment momentum is here to stay, but if firms are upping their employment levels, it means they have no choice but to increase prices in order to cover higher delayed costs due to tariffs, even if these tariffs have been in effect, in some cases, for a little more than a year.

The New York Fed paper points to two main reasons for justifying higher prices going forward: first, “some businesses operate under contracts with fixed selling prices and are unable to raise prices until such contracts expire, forcing them to absorb cost increases in the meantime”; and second, “some businesses reported taking a ‘trickle up’ approach to price increases, where they gradually raise prices over time rather than immediately raising prices to fully cover tariffs. This pricing strategy allows firms to avoid shocking their customers with sharp price increases while retaining the ability to accelerate price increases if input costs continue to rise. Moreover, uncertainty surrounding future tariff policies – including potential rate changes, exemptions or tariff responses from other countries – may be causing some firms to adopt cautious, incremental pricing strategies rather than making large, discrete adjustments. This behavior extends the period over which tariff-related price pressures work their way through the economy.”

If, as this research indicates, there has been a delayed response from firms to adjusting prices in the face of higher tariffs and the uncertainty they created, then, as we have argued during the past year, the only other alternative to control costs was to reduce and/or suspend hiring decisions. Although firms’ cost structures vary between services versus manufacturing sectors, labor costs represent a very large component of costs for firms.

This is bad news for inflation and for monetary policy

If the above is true and almost 50% of importing firms are planning to raise prices during the next year and the economy continues to face other shocks, be it because of higher oil prices or strong AI investment, etc., this is not good news for the Federal Reserve, for inflation, and for interest rates. We have argued that the Fed could keep interest rate unchanged and be patient because inflation will trend down over time. But Fed patience seems to be running short, be it because it really believes it has to do something about it or because of recent criticism or political pressure.

If we look at this week’s release of the Fed minutes from June’s FOMC meeting, the risks for higher rates have increased considerably. But as we argued after the last FOMC meeting, we think that, although Fed members’ views were divided, they decided to delay any decision until the job of the different task forces is done. However, we also said that they needed to see core Personal Consumption Expenditures (PCE) prices continue to behave. If that is not the case, our view is that Fed members are going to push for higher rates sooner rather than later. Below, we include some excerpts from the minutes to give a sense of what happened during the meeting:

1More Tariff Pass-Through Is in the Pipeline, Liberty Street Economics, by Jaison R. Abel, Mary Amiti, Richard Deitz, Sebastian Heise, and Nick Montalbano. July 8, 2026. https://libertystreeteconomics.newyorkfed.org/2026/07/more-tariff-pass-through-is-in-the-pipeline/

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.